Imperial Ginseng Products (TSXV: IGP)

Get out (leave!) right now, it's the end of you and me

Summary

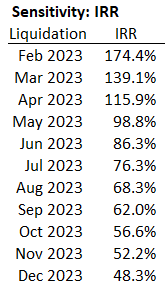

Imperial Ginseng Products (IGP) is a Canadian microcap trading at C$0.78/share with intentions to liquidate its assets, estimated to be worth C$1.34/share (fully diluted and net of liabilities). The gap between the liquidation value per share and the market price per share currently gives those willing to venture into the depths of the TSXV a potential upside of ~70%, per my assumptions. Investors don’t have to wait too long either as the wind-up of operations is expected to be completed by the end of June 2023, translating into an 85% IRR.

This is of course not without its perils as management’s track record of keeping shareholder interests at the forefront of operations doesn’t have much support.

Given the market cap of C$5.7 million, I imagine that nearly all institutions are blocked from owning and acquiring shares in IGP and furthermore, the average retail investor wouldn’t want to touch this either (that is, if they knew about it, which I suspect most do not).

The Business

Imperial Ginseng is an agricultural company farming and selling ginseng products (i.e., dried roots, seeds, fresh roots). IGP is based in Ontario, Canada, and sells its product to customers primarily in Hong Kong, China, and South East Asia.

On average, IGP focuses on harvesting 4-year-old crops although poor conditions have forced them to harvest early at the 3-year mark in the past, leaving a less saleable product. IGP tries to harvest most of its product at the 4-year mark, however, there is a market for ginseng older than 4 years and extending up to 8 years of age in some cases, with older ginseng commanding a higher price.

The business is highly seasonal with peak marketing and sales activity taking place from October to February (generally coinciding with the end of the Chinese New Year). Furthermore, as an upstream producer in the commodity space, even gross profits are highly sensitive to ginseng prices and have been negative in prior fiscal years. This is not a stable industry and we’re not dealing with a particularly good business. The sizeable number of factors and to what extent they affect annual crop yields cements the fact that this industry isn’t for the faint of heart. Here is a compilation of excerpts from their filings:

“In fiscal 2013, the Company lost all of its seeds harvested in the year because the seeds did not stratify properly due to an unusually hot period during the seed budding period.”

“Unlike previous years, the Company was unable to sell the entire harvest in 2016 as other ginseng buyers held off purchases after the largest ginseng buyer in Hong Kong, whose influence on the ginseng market and prices, ran into serious financial difficulties…”

“The company, along with most other ginseng farmers in Ontario, was hit hard by this late frost resulting in a need to reseed some of the younger gardens. The company estimates that it lost approximately 70% of this year’s seed due to this frost damage.”

“As reported in August 2016, approximately 85% of the Company’s stratified seed inventory, with a cost of $600,000, had rotted and was considered unusable.”

“The decrease in the yield per acre this year was primarily the result of an extremely wet summer in 2019 which has resulted in most growers reporting a 25% to 30% decrease in yields from the prior year.”

IGP has existed since 1989 and it’s both baffling and commendable to have been competing in this industry for so long! But now, onto the fun part.

Goodbye Ginseng Industry and Hello Liquidation!

When COVID-19 hit, operations took a turn for the worse:

Only 1/3 of the temporary foreign workers IGP applied to have in Canada made it through travel restrictions in 2020.

14-day isolation periods reduced utilization for incoming workers.

Ginseng exports to China were halted during the onset of the pandemic.

When China’s restrictions were eased, retailers were oversupplied because consumers didn’t have access to stores selling ginseng.

Ginseng prices dropped to $7.70 in mid-June 2020 (average selling prices were ~$32 in 2018 and ~$20 in 2019).

Labor shortages continued throughout 2020 and continue until this day.

Supply chains remain as knotted as the earbuds you briefly left in your pants pocket.

Civil unrest in Hong Kong, a primary destination for ginseng exports, put strain on selling and marketing activities.

On top of all of this don’t forget that during 2020, tensions between China and North America were already subject to stressors due to the US-China trade war and the detention of Huawei’s CFO in Canada.

Ultimately, the majority of these factors came to a head and in May of 2020, the Board decided to cease future crop planting activities and instead, focus on harvesting existing crops. Subsequently in October of 2020, the Board decided that all young (1- and 2-year-old crops) would be abandoned, and by FY22, IGP would harvest its final batch of matured crops and exit the industry. This timeline has been pushed back to FY23 as the company needed more time to sort out its last batch of crops for harvest, hoping to sell 5-year-old crops which garner a higher price instead of 4-year-olds.

Valuation and Assumptions

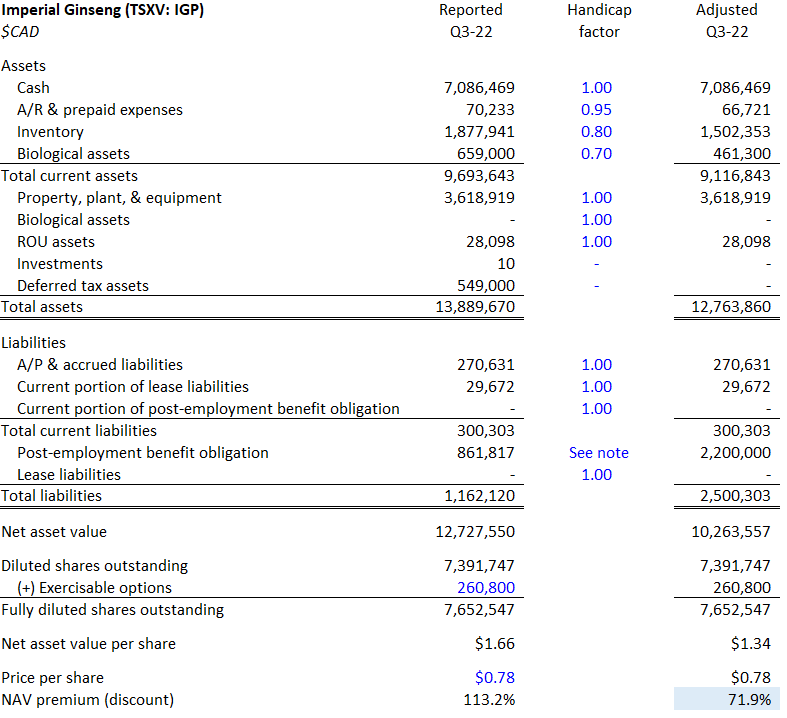

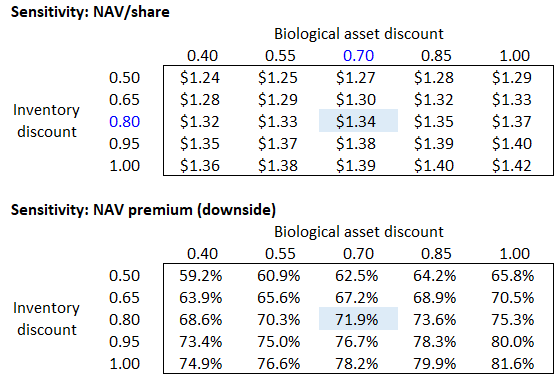

Below, you will find the state of the balance sheet as of March 31, 2022, or Q3-22. You will also find my estimate for the net asset value per share after handicapping various assets. After these adjustments, I arrive at an estimated C$1.34/share net asset value, representing a ~70% upside to market prices.

A/R and prepaid expenses. There aren’t any listed disclosures about offsetting allowances for bad debts so I’m shaving off some of its reported value for conservatism.

Inventory. Given that peak selling season is over in CY22 and April-June (i.e., Q4) sales only comprise a small portion of full-year sales, the bulk of inventory will have to be sold in Q2-23 and Q3-23. Furthermore, the ginseng market is especially challenging as of late, as evidenced by the low root prices, and it would be likely that future customers will require further enticing with free products as was disclosed in the most recent Q3-22 filings.

Biological assets. The company has ~45 acres left to harvest this fall and assuming that it yields 2,800/lb, IGP will add 126,000 lbs worth of inventory this fall. Further, if I assume that the average price of existing inventory is C$10, then I can guess that current inventories hold ~180,000 lbs of ginseng. Combining current and future inventory, I arrive at ~306,000 lbs of product.

Looking at the first nine months of recent fiscal years (July to March, because peak selling season ends in ~February), IGP was able to sell 319,000 lbs in FY19, 318,000 lbs in FY20, 594,000 lbs in FY21, and 260,000 lbs in FY22. Management commentary stands out in FY22, highlighting a big deterioration in market conditions, but it wouldn’t be a monumental hurdle to overcome to assume that the calculated ~306,000 lbs of inventory is sold by the end of next year. This also doesn’t account for the likely, albeit small, contribution of the Q4-22 (April to June) selling period. So perhaps my handicap factor is too penalizing and take these value with a grain of salt but 1) the industry has been quite challenged over the last three years, and 2) no one can predict what weather patterns in Ontario bode for this year’s harvest.

Investments. I assume the fair market value for this is zero considering that it consists of holdings of Knightswood, a subsidiary of the company. Agree or disagree, it’s immaterial on a per-share basis anyway.

Deferred tax assets. Arising due to the differences between tax accounting and IFRS accounting, this is not a physical asset that can be sold or collected. Should IGP turn a pre-tax profit in the future, this can be used to offset incoming tax expenses leading to higher cash inflow, leaving some room for upside to my NAV calculation.

Post-employment benefit obligation. This is a promise to pay critical employees a lump sum if they stay until IGP exits the industry and winds up operations. It currently sits on the balance sheet at the discounted value of its future C$2.2 million payout liability.

Exercisable options. See note 16 in the Q3-22 financial statements. 260,800 options are available for exercise with an average exercise price of C$0.26. I assume full exercise.

If you want to tamper with these assumptions yourself, feel free to contact me (goldridgecap@gmail.com) and I would be glad to share my spreadsheet. I have also used sensitivity tables to explore potential outcomes.

Risks

Firstly, I believe the primary risk is that of governance and the capital allocation of management. In terms of governance, management and the board are intertwined via cross-holdings and directorships. Not to mention that on January 13, 2021, when IGP was trading at ~C$0.30/share, that management granted themselves the option to buy 326,000 shares at an exercise price of C$0.26/share, expiring June 2023. 7 days later, they canceled 182,000 options at an exercise price of C$0.85. Now that’s just a textbook example of poor governance and the transfer of wealth from shareholders to management. Luckily this thesis isn’t predicated upon the business surviving and generating sustainable profits for shareholders.

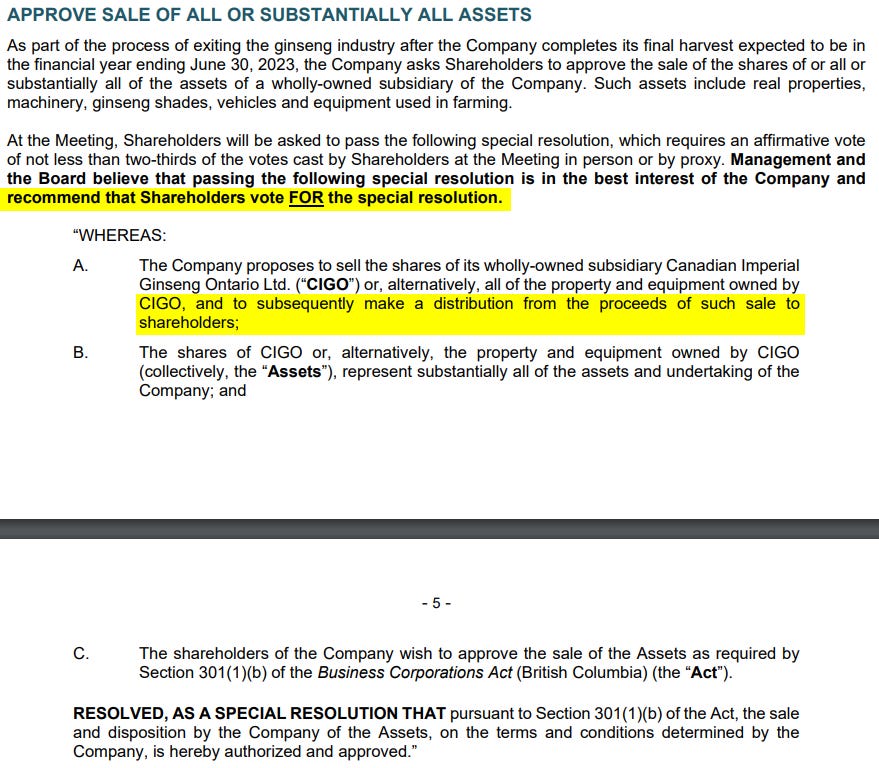

In terms of capital allocation, disclosures in the MD&As don’t explicitly state that the proceeds of liquidation will be distributed to shareholders. However, the proxy form released in November 2021 noted a special resolution proposing the liquidation of all the property and equipment followed by a distribution of proceeds to shareholders. The board and management recommended shareholders vote for the resolution.

Note that Section 301(1)(b) refers to the Business Corporations Act found here, and states that “A company must not sell, lease or otherwise dispose of all or substantially all of its undertaking unless…(b) it has been authorized to do so by a special resolution” (emphasis mine).

As for the results of the vote, it’s an unfortunate cliff-hanger because since then, there have been no filings or press releases on the outcome of the vote nor the re-appointment of the Board (not that they ever released these results over the past few years). There have only been repeated wordings in subsequent MD&As saying that “the Company’s goal remains to generate the highest possible end value upon the Company’s exit from the ginseng industry”.

Ultimately, while I would not trust management in other scenarios, I do believe that for this brief moment, management is aligned with shareholders. The board recommended that shareholders vote for the special resolution (i.e., in favour of the liquidation) and continues to disclose that its goal is to exit the industry at the highest terminal value. To the benefit of insiders, Stephen McCoach (CEO and Chairman) and Maurice Levesque (Executive VP and Director) beneficially own ~49% of the company and if my calculations are correct, this unwinding process could benefit them to the tune of ~C$4-5 million. Given another year of working through the operations of a dying company with a seemingly paltry combined salary of ~C$460,000 or getting a nice payout worth potential multiples of that, I think I’d choose the latter.

Secondly, the company intends to harvest its remaining crops in September with the selling season generally lasting until Chinese New Year (i.e., late-January/early February 2023). Should the company be unable to deplete its inventory, it could be forced to take a loss on that inventory, reducing the potential payout, or it could wait longer to try and liquidate, depleting potential IRR. Furthermore, root prices could fall even further. In Q3-22, IGP had to entice buyers with free products. Lower market prices could impair biological assets further and reduce future liquidation values. The good news is that a good chunk of the balance sheet comprises cash.

If there’s one way to sum it up, I think my friend put it succinctly when they said “Liquidations are tricky, they always take longer than you expect them to, and you always get a little less than you expect as well”.

Conclusion

Ultimately we have an equity trading at a discount to its tangible NAV. The discount (and the upside) ranges from between ~65-75% based on my assumptions, and given the estimated closing by the end of June 2023, investors don’t have to wait too long to get their money back. In my view, the distribution of liquidation proceeds is of course, the best way to maximize shareholder value, however, the risk of further difficulties liquidating assets and a tumultuous ginseng market remain.

The opportunities to acquire shares are sparse, with daily trading volume averaging close to 2,000 shares however, there is still some time to build a position as I believe that the probability of the liquidation completing before February 2023 is highly unlikely given the seasonality of the business.

Unfortunately, I anticipate that for most of those reading this, this idea will not be actionable for you, but I could not help myself from documenting some part of it.

I have no position (yet).

Disclaimer: Nothing on this blog should be considered investment or financial advice; please check out the full disclaimer here.

First of all, thank you for your detailed analysis regarding this cigar butt investment.

Secondly some considerations:

- Regarding teh NAV calculation, you are using in some cases, items in the Asset side of the Balance Sheet, that are calculated using present value / discounted cash flows to today's dollars.

For example: the case of biological assets. Acoording to the IAS 41 and the note 8 of their Annual Report FY 2022 ended in June 30: Bio assets are measured at fair value less cost to sell (meaning the expected price that we will obtain for selling the harvest less cost atributable to grow the crops until harvest less trasnactions costs to sell, based on some assumptions). This implies that the future value in nominal terms of cash to receive in future is larger than the Bio Assets Reported ammount in the BS assuming assumptions are correct.

- So when you calculate the NAV, you are subtracting biological assets in PV terms from liabilities such as Post-employment benefits which you handicaped to future values (2.2M). So when you do this, I think you are understimating cash generation of assets compared to liabilities. (Correct me if I am wrong).

-I understand the future NAV as the liquidation cash that will be obtained from liquidating the assets for cash and pating the liabilities using cash in the day of liquidation (Around finals FY2023 or 2024). So to calculate the real/precise NAV premium or discount I think that all assets/liabilities should be compounded to FV and then discounted back to PV terms to makethe comparisson with price.

The fact that you are using PV terms for assets and FV terms for liabilities, IMO make your analysis overconservative which is good because it expends yout margin of safety. Did you decide this on purpose or because of the dificulty to project the future cash flows from assest??

Thirdly, regarding the liquidation process, dou you if the cash collected will be distributed as a dividend and will be delivered to each sharholder?? Because if it is this way, a foreign investor that receives this will pay dividens to the canadian tax authority and could be possible that dividend less tax is lower than price per share paid...

Thank you, I think that I did not explain myself very well, if you have some dubts respond me please.